Do you want to be invested

in the stock market this September?

Our viewpoint

25 August 2022

Monday 22 August saw a fall in excess of 2% in the S&P 500 – is this an omen? Of course, equity markets are known for having good returns over long periods of time, and plenty of volatility over shorter time horizons. Many questions spring to mind, including: Is there any pattern to these movements, and in particular is there a pattern that investors could use to improve their returns? Put another way, should I get out of equities this week, and avoid a September Shock?

‘Sell in May and go away’ is an adage in the financial world

The message hints at the idea that the stock market has predictable annual cycles that investors should be aware of. Many people believe that the market slumps in the summer, perhaps due to senior analysts taking time off from work; others believe that the market delivers higher returns around the end of the year. Whilst these have often been cited as a rumoured annual cycle, does the data support these theories? How should this affect decision making? Is it too late to sell, before September begins?

An analytical approach

We set out to see which months of the year averaged the highest returns. To do this, we looked at data from the S&P 500 from 1950-2017, considering the return from the open of a month to the close.

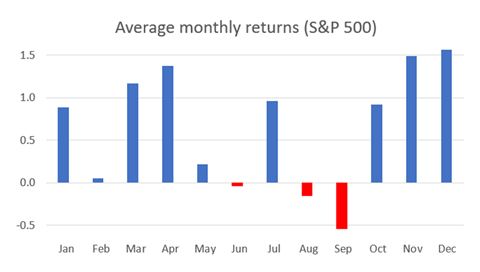

In the graph below we show the average return in each month we found from a simple face-value analysis:

(Average monthly return over 68 months)

December leads the way as the month that historically has delivered the highest average return, returning an average of 1.6%. Is it a coincidence that December has long had a reputation as a good month? On the other hand, September has delivered negative returns of -0.5%, the lowest of all the calendar months and again this accords with the old adage.

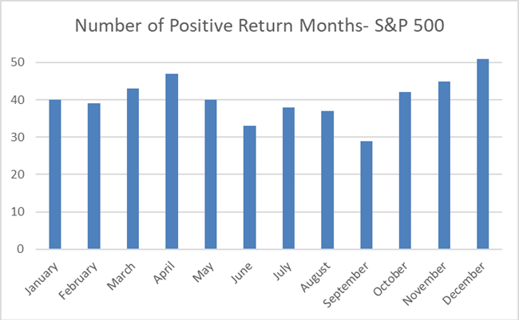

Interestingly, not only are these the months with the most extreme positive/negative returns, but they are also the most frequently positive/negative months, by number, too. This is demonstrated by the chart below, which shows that there are only two months that have fewer than 34 positive months – which means you get a negative return more often than not – those months are June and September.

(From a total of 68 months)

It’s worth noting that this is not an academic paper, and we did make a few simplifications. Most notably we didn’t allow for when stocks went ex-dividend, which will clearly have an impact. However, the 2% drop on Monday 22 August was not driven by dividend announcements!

Checking if this was merely a temporal anomaly, we looked at the data set in two halves: 1950 – 1983 and 1984 – 2017. The S&P 500 data show that September averages negative in the first half, and the lowest average return of all months in the second half of the data, in addition to the lowest number of months with a positive return.

A holistic approach

To take a more holistic look at how the market performs, we also wanted to have a look across a few other equity markets to see if this phenomenon carried across continents. The FTSE350 data across the last 20 years also provided us with evidence of negative average returns in September, although lower in magnitude (at -0.2%). Whilst September does not come out as the worst month in the UK, it is followed by a strong run of 2.9% across October – December, perhaps suggesting that being in the market from some point in October is more lucrative. Perhaps things are changing though, as the FTSE100 data since 2010 suggest a slightly positive average September figure of 0.1%, but again a strong run up to the end of the year, with a 3.9% quarterly return in the 3 months October-December.

There seems to be some seasonal impact in equity markets, supported by the data we have seen. However, of course it depends on the preference of the investor and how else might the money be invested. Also, might the recent 2% drop be reversed, and lead to a better September than ever in 2022? This is precisely what happened after a particularly bad August in 2010 - we shall see if history repeats itself!

And the results suggest

Overall, it does seem that the 4 months after May (including September) do not historically return very high figures: with June, August and September averaging below 0%. So investors with alternative investment opportunities maybe better off investing elsewhere during this period.

In conclusion, historic data suggest that four summer months after May are a bad time to be invested in equities, unless dividend payments can make up the differential; whilst the 3 months at the end of the calendar year seem to do better, returning 2.9%-3.9% across the markets we looked at. A large part of the reason for the low return after May is due to September in particular, and so perhaps the new adage ought to be “Out in August; Okay by October” – and avoid a possible September Slump in 2022?

(This blog is an opinion piece by Alex Waite, and should not be relied upon as investment advice.)

LCP on point

Shining a light on issues behind the headlines

LCP's on point papers take a closer analysis at news and issues on the UK pensions and finance agenda

Explore our papers