Finding the right

balance in VPAS

Our viewpoint

14 February 2023

Next year, manufacturers of branded medicines will be forced to return over one quarter of UK sales revenue to the government.

The repayment is a condition of membership to the Voluntary scheme for branded medicines pricing and access (VPAS), which aimed to support innovation and promote patient access to new medicines whilst helping to contain growth in the NHS medicines bill.

Industry representatives have since spoken against the rebates, stating that such a substantial repayment could lead to a significant disinvestment in the United Kingdom and that the scheme is actively undermining the aspirations set out in the Life Sciences Vision.

VPAS is a voluntary agreement entered into between the Department for Health and Social Care (DHSC), NHS England (NHSE), and the ABPI (The Association of the British Pharmaceutical Industry). The scheme began in 2019, taking over from the existing Pharmaceutical Pricing Regulation Scheme (PPRS), and is set to be re-negotiated in December 2023. The voluntary scheme is an improvement on the PPRS as it contains additional initiatives to improve patients access and healthcare services whilst ensuring financial predictability for the NHS. The current voluntary scheme aims to benefit both drug manufacturers and the UK healthcare system by striking the correct balance between the following:

- Improving patient access to medicines by getting the best value and most effective medicines into use more quickly.

- Keeping the branded medicine bill affordable and predictable for the NHS through a cap in growth of branded sales.

- Supporting innovation and a successful life sciences industry in the UK.

Drug manufacturers can join the scheme to benefit from the collaboration between the DHSC and NHSE as committed in the VPAS agreement. The agreement stated that the collaboration will, in turn, lead to earlier engagement and uptake support for high value medicines, faster NICE appraisal, and improved health outcomes. To support innovation, manufacturers which introduce new active substances (NAS) are exempt from paying the rebate applied to the sales of the NAS for the first 36 months. Companies which do not join the voluntary scheme and launch a medicine in the UK are subject to the non-voluntary, statutory scheme, which is subject to (often higher) rebates and do not benefit from exemptions. In 2019, 172 drug manufacturers agreed to the VPAS scheme.

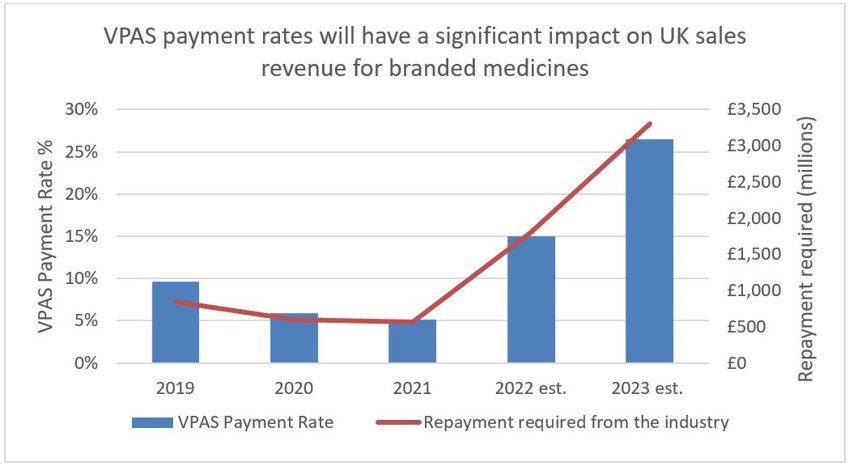

It is the second aim of affordability where the rules of membership are turning less favourable for drug manufacturers. To ensure predictability, NHS medicine spending is capped at a maximum of 2% each year. Any spend over this 2% must be reimbursed to the DHSC by the drug manufacturers. In 2023, the reimbursement percentage is to be set at 26.5%, after averaging at 7% between 2019-2021. The cause of these soaring rates is multi-factorial. Government calculations do not delve into the specifics, however, it is likely due to: increased medicine spending to tackle the Covid-19 pandemic, an uptick in demand for the healthcare system – a long-term side effect of the pandemic -, and the approval of multiple high-cost innovative therapies. An additional cost burden is the deferment of the 2022 rates which were capped at 15% after the government intervened to reduce the predicted rates of 19.1% following increased spend on medicines during the pandemic. The remaining 4.1% has been added to the 2023 bill.

Figure 1

Source: ABPI

Figure 2

Source: ABPI

Unsurprisingly, this clawback rate has sparked a negative response from the pharmaceutical industry, which is set to pay back almost £3.3 billion of its UK sales revenue. The ABPI has highlighted that the rise comes at a difficult time for the pharmaceutical industry, which is also tackling inflation (not accounted for in the repayments) and an increase in corporate tax rate from April 2023.

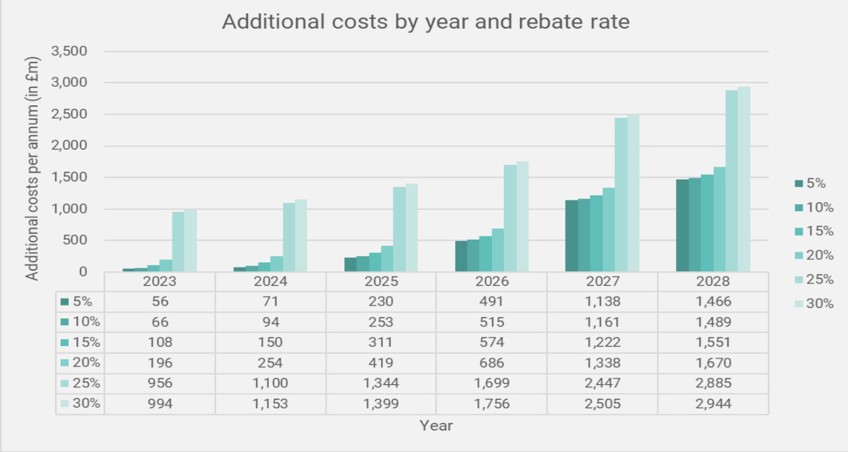

The BGMA (British Generics Manufacturers Association) has also warned that the repayments could do more harm than good to the NHS medicines bill when taken in the context of branded generics and biosimilars. The average generic is at a discount of approximately 80% to its originator, meaning the additional rates imposed by VPAS creates an environment which is “just not sustainable”, according to the BGMA. An independent analysis has highlighted the impact of the VPAS rebate on NHS savings resulting from a reduction in competition amongst branded generics and biosimilars. Ultimately, the report found that the NHS will lose out on £7.8bn of branded generics and biosimilars savings from at a VPAS rebate rate of 25-30% between 2024-2028 (Figure 3). The BGMA added that, at a VPAS rate of ~25%, “the NHS is set to lose out by more than £800m over and above the projected levy income in the first 12 months alone”.

Figure 3

Source: A consulting report: The impact on the NHS of the VPAS levy on branded generics and biosimilars

The situation escalated at the start of 2023, with Eli Lilly and Abbvie announced they are quitting the VPAS scheme following the announcement of the increase. The two companies will instead defer to the Statutory Scheme for Branded Medicines. The statutory scheme has historically had a higher repayment rate than the voluntary scheme, and members will not benefit from the close collaboration with NHSE and the DHSC. The move is intended to act as a warning to the UK government to highlight the damaging nature of the scheme, ahead of its renegotiation this year. Incidentally, the statutory scheme is also set to see a significant rise in the clawback rate this year.

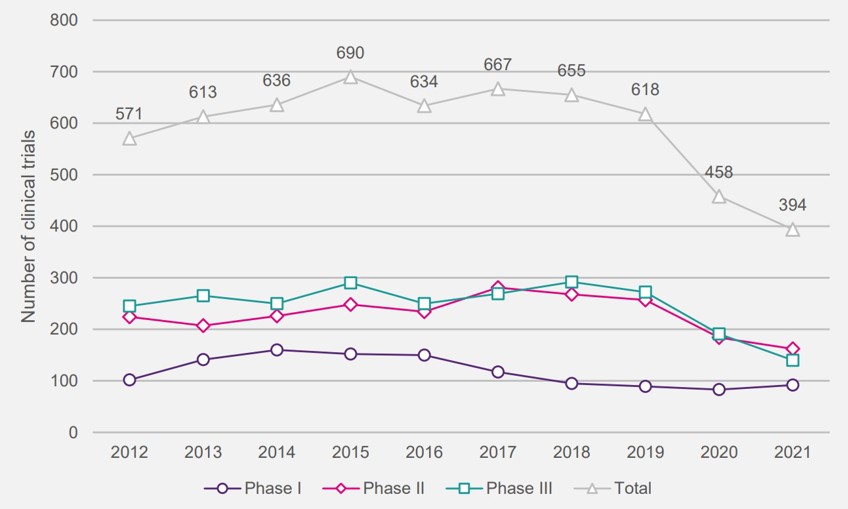

So, what does the fallout of these increased VPAS repayment rates mean for the UK life sciences sector as a whole? In its response to the publication of the 2023 rates, the ABPI suggested that it would have a significant impact on a sector which has already seen a decline in innovative research with clinical trials initiated in the UK falling by 41% between 2017 and 2021 (Figure 4). The UK has also “lost half of its global share of R&D over the last decade.” Several pharmaceutical companies, including Abbvie, have also commented that the levy rates are “not seen in any comparable country” and that “it will be increasingly difficult to advocate for the UK.” Both Bayer and Bristol Myers Squibb also suggested they will reduce their UK footprint amidst difficult market conditions.

Figure 4: Number of industry clinical trials initiated in the UK per year, by phase (2012-2021)

Source: ABPI: Rescuing patient access to industry clinical trials in the UK

The EMIG (Ethical Medicines Interest Group) recently surveyed its members, which include small R&D companies through to well-established drug manufacturers, in relation to investment intentions following the announcement of the 2023 VPAS rate, and the results were damning. 85% of respondents stated that one or more medicines would likely be moved down the launch sequence, with 10% stating that 5 or more medicines would be affected, and over 75% suggesting a 10-20% decrease in investment in UK clinical research.

Ultimately, patient access to innovative medicines will suffer as a result of the clawback. If the EMIG survey results are translated into the real-world scenario, then the UK will experience significant delays in access to novel therapies and health outcomes will worsen. The UK is already behind its European competitors, with just 68% of new medicines being available to patients between 2017-2020, compared to 92% for Germany and 79% for Italy. The current VPAS rate is only set to exacerbate this downward trend in UK life science investment.

The UK government has said that it is committed to achieving the Life Sciences Vision, set out in 2021, which aims to develop a thriving UK life sciences industry in the post-Brexit era. The current voluntary scheme ends at the tail end of this year, however, the ABPI is seeking early talks with the government to devise an entirely new settlement which “captures the huge potential of the life sciences sector to drive improvements in the health and wealth of everyone in the UK”. It is pivotal that a novel agreement addresses the issues facing the life sciences sector in the UK, and tailors the terms to look beyond cost-containment. A deepened focus on attracting innovation and improving access and outcomes, as discussed in its original aims 2019, must be revisited and further actions to fully implement them must be laid out. A new, measured agreement that equally benefits manufacturers and the government, could be a pivotal moment in promoting a healthier life sciences environment in the UK for industry, government, the NHS, and ultimately, patients.

Key takeaways:

- The VPAS scheme was designed to improve health outcomes and provide predictability of medicines spending by the NHS through collaboration between government and industry.

- The 2023 clawback rate is a substantial increase on previous years and has the potential to cause significant harm to the UK life sciences industry.

- Pharmaceutical manufacturers have indicated that this makes the UK less attractive to invest in – fewer clinical trials, less investment in UK based R&D and manufacturing facilities and potentially fewer new medicines becoming available to NHS patients.

- A new scheme is to be re-negotiated for December 2023. It is pivotal the new scheme equally benefits both manufacturers and government to revitalise the UK life sciences industry.

How life sciences can address the greatest health challenges and reduce inequalities

Health Analytics report

Explore our report which sets out how the life sciences sector has a unique opportunity to actively reduce health inequalities.

Read now