‘Retirees need

to ‘look under the bonnet’ before investing’

Media centre

17 March 2021

Since the introduction of ‘pension freedoms’ in 2015, pension savers have been free to use their pension pot as they wish and are no longer forced to buy an annuity.

As a result, annuity sales have slumped, whilst the number of people going on investing into retirement via a drawdown product has increased sharply. But the FCA became increasingly concerned that consumers who do not have a financial adviser were not choosing a suitable product in retirement and were too often ‘sleepwalking’ into having their money invested in very low return cash funds.

In response, since 1st February 2021, pension providers have been required to steer investors down ‘investment pathways’. Savers answer a simple question about what they plan to do with their money and the provider then offers a fund that they think best matches the investor’s intentions.

New research from consultants LCP shows that the good news is that charges on these ‘investment pathway’ funds are proving to be relatively modest.

But LCP have also found that there is still very substantial variation in charges between providers and also that the types of product being offered vary considerably, even for people on a single ‘investment pathway’. As a result, they are urging savers to ‘look under the bonnet’ of the different products they are being offered and think carefully before selecting the right one for them.

Commenting, LCP Partner Dan Mikulskis said:

“Freedom to choose what to do with your pension pot is a good thing, but too many people are at risk of getting poor outcomes. The new ‘investment pathways’ are welcome where they have helped to put downward pressure on charges, and could help steer consumers towards the right product. But our research has shown that different providers vary hugely both in what they will charge and in the product they will offer to the same individual. Savers need to look under the bonnet to see how their money will be invested before they choose where to save, and they need to avoid the risk of investing too cautiously given that retirement can easily last for several decades”.

What the research found

Focusing on the main investment pathway for those going into drawdown – known as Pathway 3 – LCP found:

- Of the 8 providers listed on the Money and Pensions Service comparison site in February 2021, the average charge quoted for a £100k pot was 0.64% in year one.

- Charges varied considerably from provider to provider, with the cheapest charging 0.39% and most expensive 0.93%.

Full figures are shown in the Table

| £100k investment | £100k investment | |

| First Year Charge | % | |

| Aviva | £521 | 0.52% |

| Fidelity | £725 | 0.73% |

| Hargreaves Lansdown | £752 | 0.75% |

| Interactive investor | £485 | 0.49% |

| L&G | £553 | 0.55% |

| Pension Bee | £934 | 0.93% |

| Scottish Widows | £393 | 0.39% |

| Standard Life | £732 | 0.73% |

| Average | 0.64% |

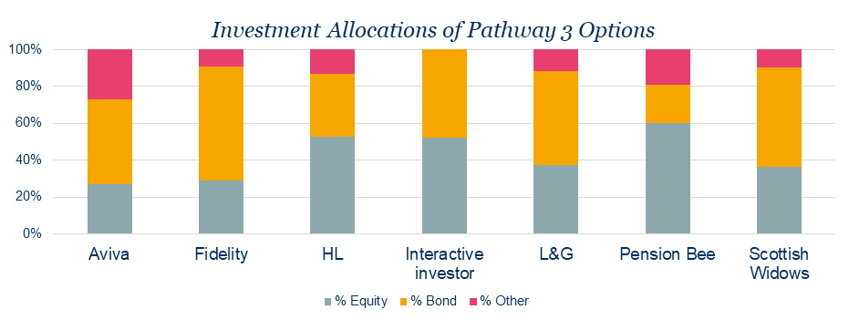

But LCP also found that pension providers are given considerable freedom by the FCA in what product they offer to match each ‘investment pathway. As the chart below shows, the investment mix can vary greatly from provider to provider, with the share invested in equities ranging from 27% to 60%.

Source: Provider factsheets and website as at end Jan 2021

LCP are concerned that a low allocation to equities can produce poor outcomes over a long retirement and that even the most heavily equity-based product on offer to these savers might struggle to sustain the kind of regular income that retirees will be looking for. More analysis can be found in the LCP research paper “How QE broke the 4% rule”.

Looking at past performance of these funds, LCP found:

- Of the 4 providers where 3-year performance was available this ranged from 2.2% p.a. to 4.6% p.a.

- Comparative tracker funds would have returned 4-5% p.a. over that period

To help to explore these issues (and answer other questions), LCP have today released a new modelling tool which estimates the impact of charges and other factors on pensions in drawdown. The tool can be found at: https://wealthtools.lcp.uk.com/

Our investment thinking

Insight hub

The latest recommended reads from our investment experts. From in-depth guides to quick-to-read blogs, we explore a range of themes to help you keep up-to-date.

Enter the hub