British Energy

Security Strategy: What might it mean for infrastructure investors?

Our viewpoint

26 April 2022

Over 2021, gas prices soared by more than 200% and coal prices by more than 100% leading to a cost of living crisis in the UK. In response the Government released its “British Energy Security Strategy” (“the Strategy”) which promised “secure, clean and affordable British energy for the long term”.

The Strategy signals that renewables (primarily offshore wind) are fundamental to delivering reliable power to the UK in the long term. It also emphasises that nuclear is a key feature of the mix, and highlights support for other transition infrastructure like energy storage.

In this blog we explore what the Strategy may mean for longer-term investors (like pension schemes) looking to increase allocations to infrastructure. We focus on lower risk ‘core’ infrastructure, targeting returns of c.8‑10% primarily comprised of stable, reliable income. In general, we believe that the Strategy (alongside a myriad of equivalent announcements in the EU) provides further momentum to establish renewable energy investments as part of investors’ ‘core’ infrastructure allocations.

What are some highlights for investors?

LCP’s Energy Analytics team has provided a summary of the Strategy and what it means for the UK energy market here.

The Strategy states that “by 2030 we will have more than enough wind capacity to power every home in Britain”, setting the ambitious target of increasing offshore wind capacity from 13GW to 50GW by 2030. This is the clearest indication that the government expects offshore wind to form the backbone of our power generation over the long-term. Offshore wind is often the preserve of the very largest infrastructure investors due to the typical asset sizes. These projects are also highly sought after, meaning yields (and therefore expected returns) are generally lower. To date, this has meant it has been hard for many commingled infrastructure funds to access offshore wind, and we expect this trend may continue. Similarly, despite the government’s positive stance on nuclear energy, we do not expect to see nuclear projects entering core infrastructure portfolios any time soon as these are also very large, expensive and complex.

The Strategy indicates that the government expects onshore wind and solar PV to be an important part of the UK’s energy future, although offshore wind and nuclear is clearly its focus. There is ambition for a five-fold increase in deployment of solar PV by 2035, although nothing new for onshore wind (more on this later). Despite this, onshore wind and solar PV has been – and we anticipate will continue to be – a mainstay for managers looking to include renewables in their ‘core’ infrastructure portfolios.

Over the last decade solar PV and onshore wind have become well established and costs of producing power have fallen dramatically. Their popularity has led to more players entering the market, which has compressed yields for operating assets. We expect, therefore, that in addition to buying operational assets, managers will begin accessing projects at an earlier stage to earn a “construction premium” and enhance expected returns. This does, however, introduce an additional element of risk so it is important to find specialist managers with experience working with developers. It is also important that managers investing in “core” infrastructure can find assets generating reliable cashflows. As new solar and onshore wind investments are exposed to movements in energy prices over the long-term, we believe managers that look to pre-contract renewables revenues with strong counterparties, offering some inflation-linkage where possible, will be more in favour.

The Strategy also made supportive comments with respect to developing technologies such as green hydrogen and energy storage (batteries), which we believe may be a catalyst for these newer areas. Presently, these technologies are generally considered to be too early stage for ‘core’ infrastructure portfolios, but this may change as policy framework and business models are developed to underpin investment over the next few years. Whilst today they might appeal more to investors with a higher risk appetite, they may well follow the path of onshore wind and solar into ‘core’ portfolios as they become more established, especially with the support of governments (in the UK and elsewhere) who want to bring large scale deployment forward. LCP’s Energy Analytics Team has given a detailed view on the outlook for UK battery storage investment here.

Taking a more global view

It appears that political pressure from some UK MPs meant no easing to planning regulations for new onshore wind development. This highlights a prominent risk with infrastructure investment generally – policy action (or inaction) and market signalling. Long-term, illiquid investments like infrastructure are influenced by changes in government policy, favourable or otherwise, over the life of an asset. For this reason we tend to advocate a global approach for ‘core’ infrastructure – including renewables - as this helps mitigate policy risk by providing exposure to a broader range of funding mechanisms and regulatory regimes. We also support diversification across a range of different infrastructure sectors for the same reason.

Not only this, but a multi-jurisdiction approach provides investors with a much larger opportunity set. For example, the EU has recently taken a very supportive stance on renewables (in part because of some member countries’ reliance on Russian gas), which we believe has created a favourable investment landscape for investors. The trend of accelerating decarbonisation and reducing reliance on fossil fuels is global, and we believe investing across jurisdictions gives access to a broader spectrum of opportunity.

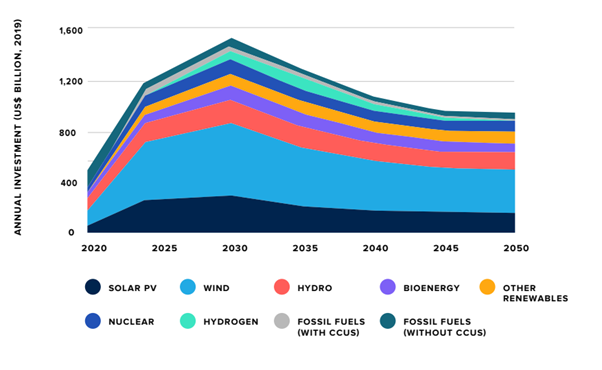

Figure 1: Annual global investment required to reach Net Zero (US$ billions)

The Net Zero transition will be the single greatest investment theme of the next 30 years. In the same week as the government released its Strategy the IIGCC1 released its Climate Investment Roadmap outlining investment required in renewables, and other technologies, to achieve global Net Zero ambitions. The numbers are staggering. The report states that “installed renewable generation must increase 80% in the next decade” to satisfy new demand for electricity and replace fossil-fuels. Importantly, as highlighted by the chart from the Roadmap, traditional renewable generation technologies in solar PV and wind (predominantly onshore wind) around the globe are expected to play a key role in achieving Net Zero. This highlights the growing opportunity set of renewables investments for ‘core’ infrastructure managers, in the UK and elsewhere. Over the coming years we expect to see renewables and other transition infrastructure increase in prominence in managers’ portfolios.

References

[1] Institutional Investor Group on Climate Change

Quotes are from: https://www.gov.uk/government/publications/british-energy-security-strategy/british-energy-security-strategy

Chart is from: https://www.iigcc.org

Our investment thinking

Insight hub

The latest recommended reads from our investment experts. From in-depth guides to quick-to-read blogs, we explore a range of themes to help you keep up-to-date.

Enter the hub