Why Trustees should get interested in interest rates - our insight into the current macroeconomic challenges facing sponsors

Our viewpoint

26 September 2022

This blog series reflects on recent global economic trends, and what these could mean for defined benefit pension schemes.

In this blog, Francesca Bailey and Tom Gillespie consider why increasing interest rates should be on the agenda for trustees and sponsors.

In the past few months, the Bank of England ("BoE") has been under scrutiny, accused of taking a too-prudent approach to spiralling inflation, with cautious 0.25 percentage point rises in the bank rate since December last year.

Although this tentative approach to monetary policy was understandable during a period of subdued economic growth and a likely recession emerging as we enter the final quarter of 2022, the original approach was a sharp contrast to the recent high rate-rises adopted by the US Federal Reserve and European Central Bank.

However, with inflation reaching towards double digit levels (July 2022: CPI 10.1%, August 2022 CPI: 9.9%) and further price rises assumed inevitable by the end of the year, the BoE has followed through on its pledge to take more aggressive action. The BoE raised the rate by 0.5% to 1.75% on 4 August 2022, its largest single increase since 1995, followed by a further bumper 0.5% rise on 22 September, taking rates to 2.25%, the highest level since 2008.

These rate hikes are expected to have (and indeed already have been having) significant impacts on defined benefit pension schemes, and their key stakeholders – members, trustees and sponsors.

How has the world changed?

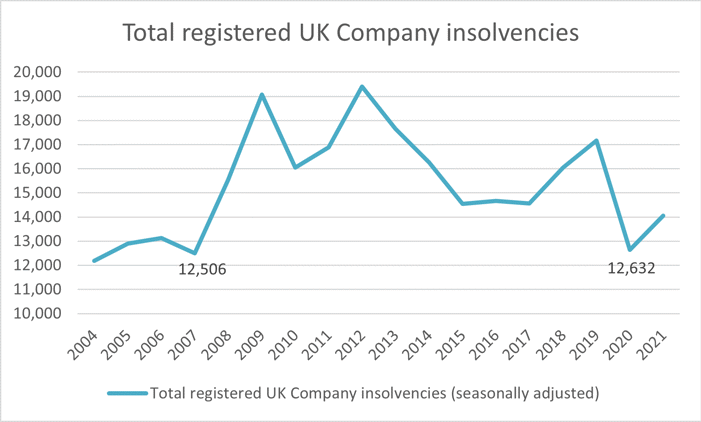

During the pandemic, organisations sought to improve their liquidity, typically turning to existing lenders to both draw down and extend existing borrowing facilities, which were available at extremely low interest rates. This allowed many businesses to remain resilient, with reported insolvencies in 2020 falling to levels not seen since before the global financial crisis.

Source: The Insolvency Service Data

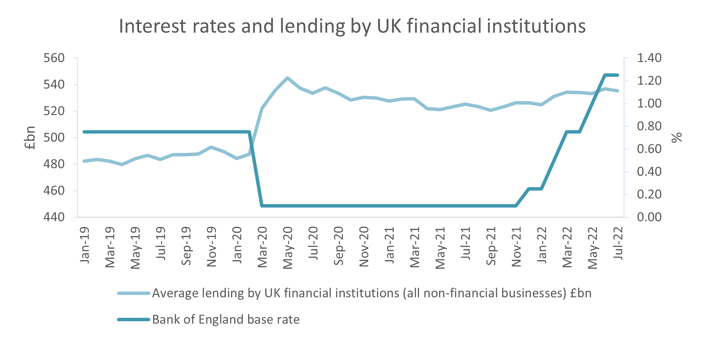

Combined with Government support, many sponsors remained resilient, albeit with an increased debt burden to service. UK Government data highlights that total UK debt across non-financial businesses is now more than 10% higher compared to the pre-Covid-19 position.

Source: Bank of England Data

With new macroeconomic headwinds being experienced (geopolitical conflict, supply chain challenges , inflation , to name a few) whilst interest rates are higher than they have been for the past thirteen years, concerns are growing about both wider business resilience and the cost and availability of credit for organisations that need to refinance.

Debt and the employer covenant

The debt structure of a sponsor is a key factor influencing covenant support. Trustees need to understand their sponsors’ current debt structure, including maturity dates, interest profile (eg fixed or floating), any covenants and, critically, how their scheme’s creditor claim ranks compared to lenders.

Importantly, any changes in this structure could have a significant impact on the covenant support available to the scheme. For example, changes in the cost of debt could impact an employer’s ability to provide financial support to its scheme (as financing debt becomes more expensive) and changes in the security provided to lenders could impact a pension scheme’s insolvency recovery. Independent covenant experts can help with both understanding the baseline position (trustees should expect that this information is covered as part of any triennial covenant assessment), and the impact of specific refinancing exercises on a scheme and sponsor.

All pension scheme stakeholders should be mindful of the impact of corporate events. This is because, since the introduction of the Pension Schemes Act 2021, if suitable mitigation is not provided to a scheme that experiences material detriment because of an event, related parties (which includes directors, sponsors, trustees and even lenders) could find themselves subject to civil or financial penalties.

The Pensions Regulator is keen to remind trustees and sponsors of the importance of risk management on this topic. In August David Fairs, Executive Director of Regulatory Policy, Analysis and Advice at the Pensions Regulator released a blog, which set out in detail TPR’s expectations for trustees and sponsors in the event that refinancing activity takes place.

This highlights the importance of engagement. Processes should be in place to ensure that any changes in a sponsor’s financing profile is communicated in a timely manner, and that sufficient information is shared to allow the covenant impact of these to be assessed. This could be through a regular covenant monitoring process or information sharing agreement.

An integrated approach remains key

Beyond potential impacts on sponsors, rising interest rates impact DB schemes in a variety of ways.

Rising yields will mean lower liability values. It will also mean hedging assets fall in value (and can mean potentially significant cash calls on LDI holdings), though from a funding perspective the net impact is typically positive. We are helping our clients to lock in some of these gains by reducing levels of risk in their investment strategies or helping them secure some or all of members’ benefits with an insurance company (through buy-in or buy-out).

From a member perspective, rising interest rates will mean lower transfer values and could result in future changes to other member option terms such as commutation. Trustees should carefully consider the wider economic environment when making member-related decisions, ensuring effective communication, and being mindful that member experience can have a significant impact on journey plans.

All of these factors together really highlight the importance of joined up thinking. At LCP we have covenant, investment, actuarial, and governance specialists who work together, alongside our clients, to ensure that their scheme and members are in safe hands. Please don’t hesitate to get in touch to find out more.

Shifting GEARS

Key stages to success

Our new hub contains all the resources you need in one place to design, implement and evolve your strategic journey plan.

Explore the hub